Vietnam continues to maintain its status as a top-tier destination for international capital, but the 2025–2026 investment cycle has introduced a heightened level of complexity for global entrants. While the market remains “open,” the transition from opportunity to operation is governed by a rigorous regulatory environment that frequently catches newcomers off guard. For the strategic investor, success is no longer just about market entry; it is about navigating a highly regulated landscape where administrative precision is the primary determinant of deal certainty.

The Power Players and Preferred Sectors (FDI Trends)

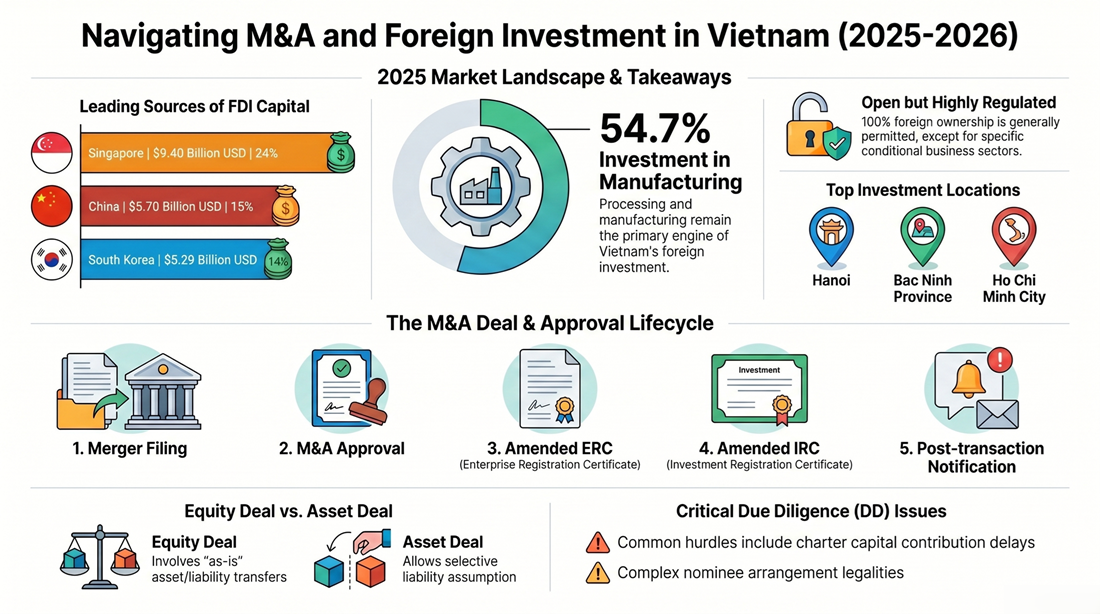

Market data from the 2025 cycle confirms a rigid shift toward administrative and industrial maturity. Regional powerhouses continue to anchor the Vietnamese economy, with Singapore leading the pack at $9.40 billion, representing a 24% ratio of total investment. This is followed by China (15%), South Korea (14%), and Japan (10%).

The allocation of this capital reveals the strategic priorities of these investors:

- Processing and Manufacturing: Dominates the landscape with 54.7% of total FDI, underscoring Vietnam’s role as a critical link in global supply chains.

- Real Estate: Remains a significant pillar at 18.51%, driven by urban development and industrial infrastructure.

- Supportive Industries: Wholesale and retail (7.9%) and science and technology (3.7%) reflect the growing sophistication of the domestic consumer market.

These figures indicate that while manufacturing remains the engine, the diversification into technology and retail suggests a maturing economy that requires more nuanced legal structuring than in previous decades.

The “Open but Regulated” Paradox

Foreign investors must reconcile a fundamental duality: Vietnam is aggressively courting investment while simultaneously tightening oversight. The regulatory framework rests on four essential legislative pillars:

- Investment Law 2025: Governs market access and conditional sectors.

- Enterprise Law 2020: Dictates corporate governance and capital structures.

- Securities Law 2019: Imposes a 50% foreign ownership cap for public companies (though relaxations exist for specific industries).

- Competition Law 2018: A critical pillar for M&A, requiring mandatory merger filings and approvals for economic concentrations.

As a legal strategist, I counsel clients to adopt the following mindset:

“Open for business…but foreign investment highly regulated”

Navigating this paradox requires moving beyond commercial due diligence to ensure strict alignment with WTO commitments, the CPTPP, and the EVFTA.

Structuring the Deal: The Hidden Weight of Equity vs. Assets

In the Vietnamese M&A context, the choice of structure is a high-stakes decision that dictates the long-term risk profile of the investment.

- Equity Deals: These are the most common but also the most complex. The buyer acquires the target company “as is,” inheriting all assets and liabilities. This necessitates exhaustive due diligence, as any historical non-compliance becomes the buyer’s burden.

- Asset Deals: These allow for selectivity, but they trigger significant operational friction. Customers and suppliers are more likely to review their dealings with new owners, and warranties are generally restricted to specific assets rather than the business as a whole. Furthermore, the assignment or novation of existing contracts and licenses can be a significant administrative hurdle.

- Offshore Transactions: This remains a preferred route for many international firms. By transferring ownership of a parent entity incorporated outside Vietnam, there is no change to the ownership and capital structure of the Target’s Vietnamese subsidiary at the local level. This effectively bypasses many local licensing procedures, though it does not exempt the parties from potential merger filing requirements under the Competition Law.

The Due Diligence Minefield (Conditions Precedent and Closing Blockers)

In Vietnam, what may seem like minor administrative details often function as absolute Conditions Precedent (CPs) or “closing blockers.” Legal Due Diligence (LDD) must focus on three high-risk areas:

- Charter Capital Compliance: Investors are strictly required to pay in full the registered charter capital within 90 days from the date the Enterprise Registration Certificate (ERC) is issued. Failure to adhere to this window is a common discovery during LDD and can freeze subsequent M&A approvals.

- Nominee Arrangements: These arrangements, often used to circumvent ownership restrictions in conditional sectors, are not recognized under Vietnamese law. Investors using local proxies have no legal standing to protect their equity, making such structures a fatal risk.

- Industry-Specific Regulatory Permits: Beyond general licenses, “sub-licenses” are deal-critical.

- Renewable Projects: Require MOIT acceptance test results before commercial operation.

- Education: Face significant challenges when converting from local to foreign-invested status.

- Pharmaceuticals: Are subject to strict drug distribution restrictions that can limit the domestic status of the target company.

The “FX Side Letter” Warning

The movement of capital in Vietnamese M&A is strictly monitored through mandated bank accounts: the Direct Investment Capital Account (DICA) for FDI and the Indirect Investment Capital Account (IICA) for other holdings.

A critical regulatory trap exists regarding currency denomination: Foreign currency is only permitted for M&A transactions where both the buyer and seller are non-resident entities. If a resident is involved on either side, the transaction must be settled in Vietnamese Dong (VND).

To hedge against currency volatility, parties often sign “FX side letters” to adjust prices. Investors must be warned: these letters have no legal validity. Such arrangements are frequently discovered by Vietnamese authorities during capital audits or when the buyer attempts to repatriate dividends. Discovery leads to administrative penalties and can jeopardize the legality of the entire fund flow.

The Long Game in Southeast Asia

Reaping the rewards of the Vietnamese market requires a strategic willingness to “budget for time, cost, and effort.” The 2025–2026 environment is characterized by specific regulatory windows that must be factored into any deal timeline:

- Merger Filings: 30 to 90+ days depending on the phase of assessment.

- M&A Approval: Typically ~1 month for acquisitions by foreign investors.

- ERC/IRC Amendments: Each takes approximately 1 to 3 weeks to process.

The regulatory environment is maturing toward greater consistency and enforcement. Those who prioritize legal precision over speed will find Vietnam a stable and highly rewarding jurisdiction.

In a market where the rules are evolving as fast as the opportunities, is your legal strategy as agile as your business model?

Contact us today to receive dedicated advice and the most suitable solution for your business!

Hotline: +84 933096426 – +84 868 591 260

Email:

Website:

Partners in Vietnam:

Contact Vietnam representative: Duc Luong Services

Hotline: +84 933096426 – +84 868 591 260

Email: ducluongservices@gmail.com

Website:

STC VN Co., Ltd.

Hotline: +84 933096426 – +84 868 591 260

Email: info@staunchlyservices.com.vn

Website: https://stauchlyservices.com.vn

No responses yet