Receiving your Enterprise Registration Certificate (ERC) is a milestone — but it is not the finish line. For foreign-invested enterprises (FIEs) entering Vietnam, the period immediately after registration is where avoidable mistakes turn into penalties, blocked invoicing, or problems during the first tax finalization.

This guide sets out the post-incorporation obligations a newly registered company in Vietnam should complete, organized by when they apply. It is written with foreign investors and their in-house finance and legal teams in mind, and reflects the regulatory framework in force as of 2026.

The key principle: obligations are triggered by activity, not all at once

A common source of anxiety for new entrants is the assumption that every obligation arises the moment the ERC is issued. It does not. Many requirements are triggered by actual events:

- Social insurance (BHXH) applies only once you employ staff who fall within the compulsory scheme.

- E-invoices must be registered and accepted by the tax authority before you issue your first invoice.

- Fixed-asset depreciation is only relevant once the company holds fixed assets.

- Sub-licenses apply only to conditional business lines.

The practical approach is to sort the tasks into four buckets: do immediately, deadline-driven, activity-triggered, and internal standardization.

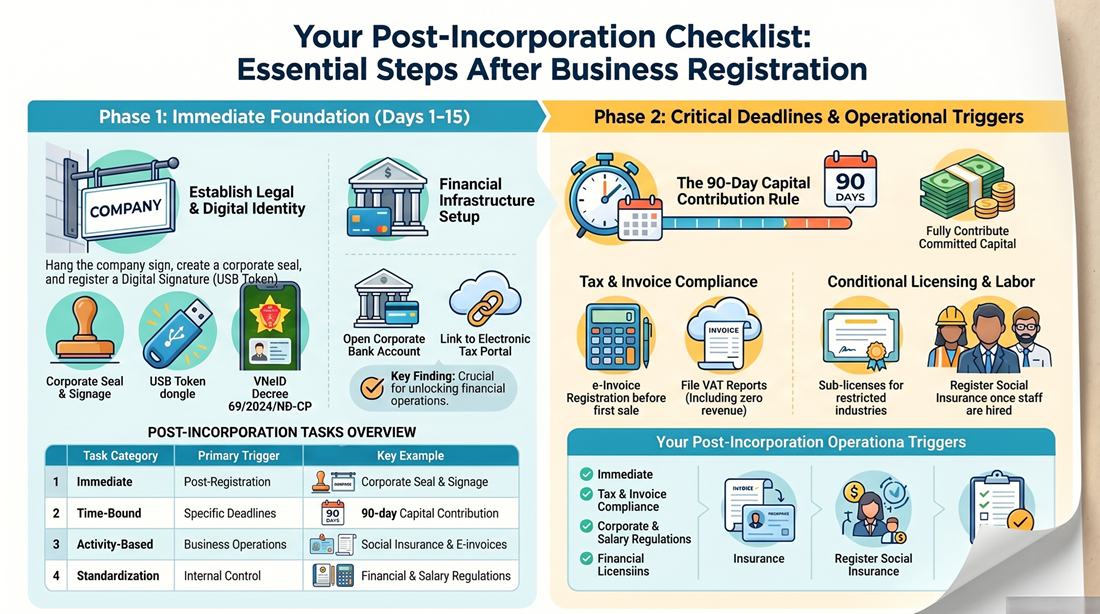

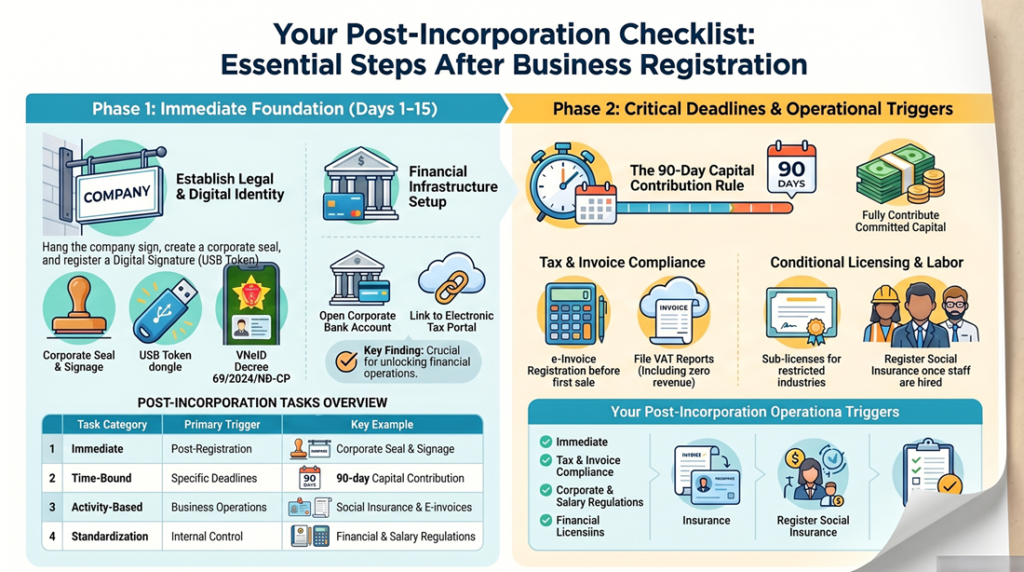

Bucket 1 — Do these immediately after the ERC

- Secure the original legal file. ERC, charter, member/shareholder register, owner identification documents and appointment resolutions. This is the master file you will rely on to open bank accounts, sign contracts, raise capital, amend your registration, or complete an M&A transaction later (Law on Enterprises 2020; Decree 168/2025/ND-CP).

- Display a signboard at the registered office. It must show the correct company name and tax code. A missing signboard — or no genuine activity at the registered address — is one of the first red flags during a tax authority site check.

- Engrave the company seal and adopt a seal-management rule. The company decides the type, quantity and content of its seal; prior notification of the seal specimen is no longer required (Article 43, Law on Enterprises 2020). Internal control over who holds and uses the seal remains essential.

- Open a corporate bank account. Never run company receipts and payments through a personal account. The corporate account is the basis for invoice settlement, capital contributions, payroll and accounting reconciliation.

- Obtain a digital signature (USB token). It is used for tax filing and payment, e-invoice registration, electronic social insurance, and signing documents online. Treat the token and password as a critical legal asset.

- Register for the electronic tax account and e-tax payment. Link your bank, and keep the responsible contact and email updated so you never miss a notice from the tax authority.

- Set up the enterprise electronic identity on VNeID. Under Decree 69/2024/ND-CP, the organizational e-ID is increasingly required for electronic administrative procedures — do this early.

Bucket 2 — Deadline-driven obligations

- Contribute charter capital within 90 days. Founding members, owners and shareholders must contribute the committed capital within 90 days of ERC issuance (Articles 47, 75 and 113, Law on Enterprises 2020). Failing to contribute in full — without a timely capital adjustment — can create asset liability and affect your financial statements, banking file and any future M&A. For FIEs, capital should generally flow through the direct investment capital account (DICA), so plan the inbound transfer early.

- Check the business license tax (lệ phí môn bài). New companies are usually exempt in their first year, but the obligation to declare and pay resumes the following year — track it to avoid an early-year miss.

- Register e-invoices before your first invoice. The old “issuance notice” mechanism is gone. Issuing an invoice before approval risks an invalid invoice and penalties (Decree 123/2020/ND-CP; Decree 70/2025/ND-CP; Circular 32/2025/TT-BTC).

- File periodic VAT returns. Even with no revenue yet, you must file on time if you fall within the monthly/quarterly filing scope.

Bucket 3 — Triggered when activity begins

- Personal income tax (PIT) filing once income is paid — keep labor contracts, payroll and payment records aligned.

- Accounting system from month one. Do not wait until year-end to gather documents (Law on Accounting 2015; Decree 174/2016/ND-CP; Circular 99/2025/TT-BTC).

- Fixed-asset depreciation only when the company acquires assets such as vehicles, machinery or premises.

- Initial labor file when you start employing staff: contracts, timesheets, payroll, labor register (Labor Code 2019; Decree 145/2020/ND-CP).

- First-time social insurance registration when you employ staff within the compulsory scheme (Law on Social Insurance 2024).

- Sub-licenses / conditional business requirements. An ERC does not by itself authorize every line of business. Sectors such as food, education, logistics, tourism, construction, healthcare and cosmetics require conditions to be met or a sub-license obtained before operating (Law on Investment 2025 and sector-specific laws).

- Branches, representative offices or business locations must be registered when you operate beyond the head office.

- Personal data protection. Once you run a website, CRM, recruitment or payroll, data-protection obligations apply (Decree 13/2023/ND-CP; Law on Cybersecurity).

Bucket 4 — Internal standardization

Adopt core internal regulations early: financial policy, spending policy, salary and bonus rules, advance/settlement procedures and a contract-signing process. These are the foundation for justifying expenses to the tax authority, resolving disputes, and controlling internal cash flow.

How ISC Global helps

Across many real engagements, one lesson stands out: assign a single accounting/legal point of contact to own this checklist and build the document folder from month one. Disciplined record-keeping from the start prevents missing documents at tax finalization, smooths bank and regulator interactions, and is decisive if the company later raises capital or undergoes M&A.

ISC Global supports both domestic companies and foreign-invested enterprises through the post-incorporation phase: compliance review, tax and accounting set-up, legal file completion, and a clean internal-governance framework from day one.

Planning to set up — or have you just set up — in Vietnam? Talk to ISC Global for a post-incorporation compliance review tailored to your sector and structure.

🌐 iscglobal.asia – iscglobal.edu.vn | 📞 Hotline/Zalo: +84 933 096 426 – +84 868 591 260

This article is for general information and reflects regulations current as of 2026. For advice on a specific situation, please contact us directly.

Contact us today to receive dedicated advice and the most suitable solution for your business!

Hotline: +84 933096426 – +84 868 591 260

Email:

Website:

No responses yet